AI Financial Advice Needs a Permissioned Data Boundary

AI financial advice should not be judged only by the answer it gives. The safer question is what data it can see, what it can do, and who can inspect the boundary.

Why this matters

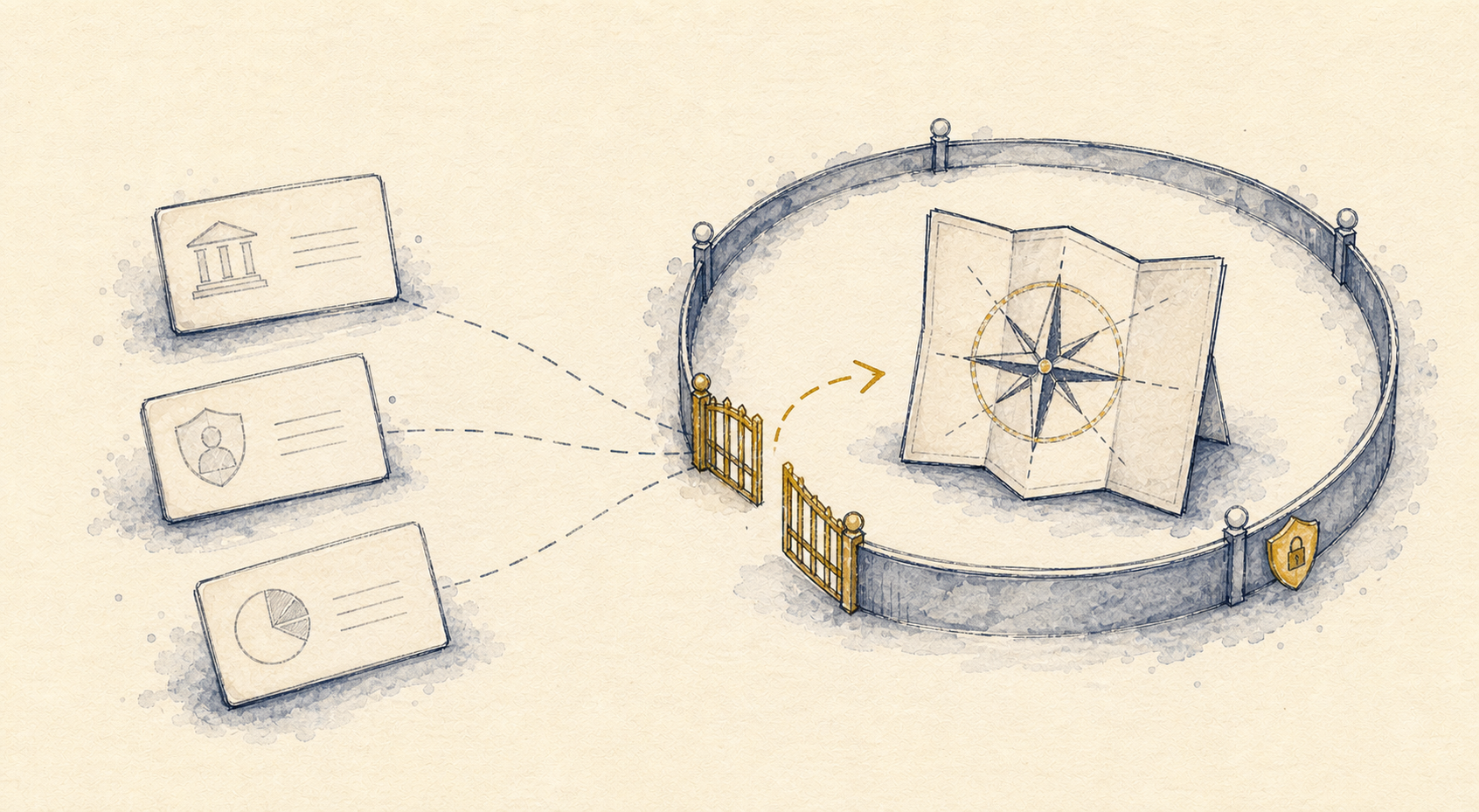

Imagine a personal AI that can see your current account, savings, investments, pension history, mortgage, salary, tax documents, insurance policies, debts, calendar, and financial goals.

It would probably give better answers than a blank chatbot.

It would also be holding enough context to do real damage if the boundary were vague.

That is the tension with AI financial advice. The more useful the tool becomes, the more sensitive the input becomes. A generic answer about budgeting is one thing. A context-aware assistant that understands your full financial life is another.

So the question cannot only be, “Was the answer good?”

It also has to be:

- what data did it use?

- what was it allowed to infer?

- what was it allowed to change?

- what did it log?

- when did a human need to review it?

That is where the permissioned boundary becomes part of the product.

Worked example

FINRA’s 2026 Annual Regulatory Oversight Report discusses GenAI risks around agents, including data sensitivity, privacy, auditability, domain knowledge, scope of authority, and human-in-the-loop oversight. Those categories are useful because they move the conversation away from vague enthusiasm and toward operating controls.

At the same time, wealth-management research from BCG and MSCI points to growing AI investment and serious interest in agentic workflows, adviser efficiency, personalization, and client engagement.

Those two things are now happening at the same time:

- AI tools want more financial context because context improves usefulness.

- Financial data requires tighter governance because the stakes are higher.

This is not a reason to avoid AI in money. It is a reason to design the boundary before pretending the assistant is safe.

Financial AI should feel like a well-permissioned workspace, not a clever stranger wandering through the filing cabinet.

A practical boundary might be boring in the best possible way.

| Boundary question | Why it matters |

|---|---|

| What can the AI see? | Sensitive data should be scoped, not dumped in by default. |

| What can it do? | Reading, drafting, recommending, and executing are different permissions. |

| What gets recorded? | Advice and actions need an audit trail. |

| Who reviews consequential steps? | Some decisions need human judgment before action. |

| How can access be revoked? | Permission that cannot be withdrawn is not much of a permission. |

This is especially important because financial advice is full of edge cases. Two people can ask the same question and need very different answers because of tax position, job security, family obligations, risk tolerance, age, location, debt, and plans they have not yet said out loud.

Context helps. Context also increases responsibility.

Limitations / not a fit

There is a cheap version of this argument that simply says “AI advice is dangerous”. I do not think that is the useful take.

AI can help people understand options, prepare for adviser conversations, organize documents, spot patterns, compare tradeoffs, and make financial questions less intimidating. That is worth building toward.

The mistake would be to treat financial AI like a normal productivity assistant with a money skin on top.

Money is too consequential for that. A tool that can summarize a portfolio is not the same as a tool that can recommend a rebalance. A tool that can draft a mortgage application is not the same as a tool that can submit one. A tool that can read a tax document is not the same as a tool that can act on it.

The product should make those lines visible.

Good financial AI will need enough context to be useful and enough restraint to be trusted. That means permissions, audit trails, domain limits, human review points, and a user who can see what is happening.

The future of AI advice may not be the assistant that sounds most confident.

It may be the one with the clearest boundary.

Sources

- FINRA: 2026 Annual Regulatory Oversight Report, Gen AI

- BCG: AI and the Future Economics of Wealth Management

- MSCI: Wealth Trends 2026